{kind=link}

The transition from operating as predominantly micro-finance lenders to being designated small finance banks was only the beginning of the challenge for some of the entities that were granted the small finance bank licence.

While the usual transition pangs were known, what came as a rude surprise was the fast deteriorating operating environment. While demonetisation was the first blow for the sector, loan waivers that brought “moral hazard” to the fore, and heightened local political interference in certain states, have only added fuel to the fire. Faced with multiple headwinds, the listed stocks have mostly underperformed. What’s the way forward – struggle and put up with the pain or get merged with a “big boy” as one of their peers is contemplating?

Why a SFB?

In September 2015, the RBI paved the path for creation of small finance banks (SFBs) and granted 10 licences. While the overt objective was financial inclusion, the rules mandate lending to customers at the bottom of the pyramid (loan size up to Rs 25 lakh have to form at least 50 percent of the loan book). The entities in return are allowed to mobilise deposits and enter into other banking activities.

In the conversion journey, in the absence of a retail liability franchise, these entities will have to resort to bulk deposits. While cost of bulk deposits (although lower than bank liabilities due to no intermediation cost) and regulatory requirements (CRR, SLR, etc.) is margin-dilutive, sticky asset pricing might help shield against margin pressure. Further, upon conversion to SFB, spread cap limit (like NBFC – MFI of 10 percent) will not be applicable. Customer base is not rate-sensitive, but more driven by service delivery.

However, they are likely to face several other challenges in the initial years of banking operations, like adapting to banking technology, raising retail deposits, adding new branches and training employees.

The two notable transition candidates are Equitas and Ujjivan Financial – both converting from a micro finance NBFC to a small finance bank. Their journey post conversion has been a saga of challenges.

Deteriorating credit discipline of MFI borrowers

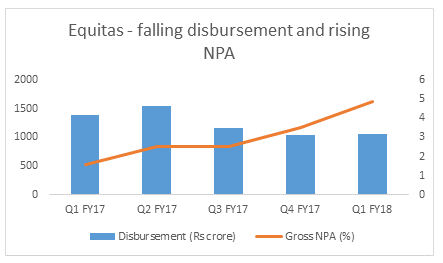

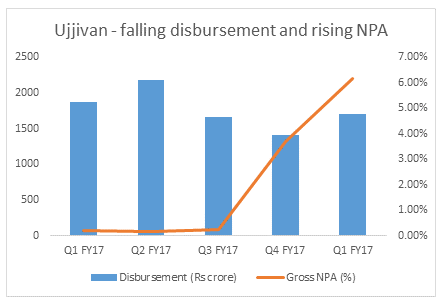

Firstly, loan growth has been on a slow lane post-demonetisation and though it is limping back to normalcy, it is yet to regain the pre-demonetisation mojo. However, the bigger challenge has been the rapid deterioration in asset quality.

Local political interference has always been a risk factor for the microfinance sector and has manifested itself in some states like Maharashtra, where local politicians have been trying to win brownie points from a local population reeling from the impact of demonetization.

There are reports of significant deterioration in group discipline (attendance in centre meetings is below 50 percent) and increasing signs of moral hazard. The spate of state elections lined up in the coming months along with the general elections in early 2019 might keep the pitch high on loan waivers. The collection officer has to then visit each member’s house separately, adding to operating expenses.

While hopes were pinned on good rains, the distribution of rains leaves little room for comfort. Finally, in an inflationary environment with tight fiscal situation a significant improvement in support prices of agriculture that supports rural prosperity shouldn’t be expected. Fiscal profligacy resulting in more money in the hands of the poor could be a wild card.

What ails Ujjivan and Equitas?

Both these well-capitalised entities have witnessed a decline in disbursal alongside a steep increase in credit cost as the asset quality deteriorated at a faster clip.

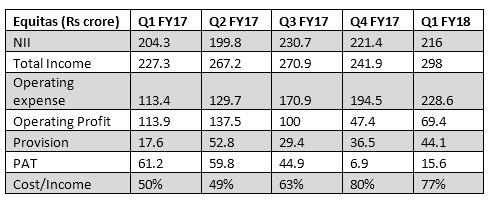

This has had an adverse impact on overall financial performance. Equitas, for instance, reported an after-tax-profit of Rs 15.6 crore in the quarter gone by, down 75 percent over the year-ago period.

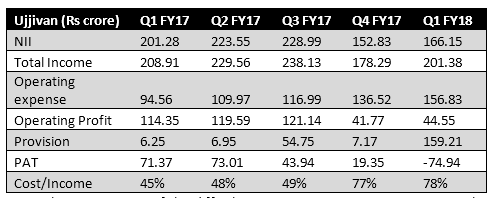

Ujjivan Financial, in fact, reported a loss of Rs 75 crore in the quarter gone by as against a profit of Rs 71 crore in the year-ago quarter.

Given the continuation of the difficult operating environment, we expect elevated credit costs in FY18 as well. Especially the coming quarter (Q2 FY18) might continue to showcase the pain, although both the entities are incrementally reporting improvement in collection efficiency as well as disbursement.

Should you look at accumulating on the weakness?

In the past one year, shares of Equitas and Ujjivan have fallen by 18 percent and 30 percent, respectively thereby significantly underperforming the benchmark that has risen by 14.5 percent over this period.

While the transformation challenges and macro environment are unlikely to change overnight, Equitas appears to be adopting a slow and gradual strategy of diversification of asset book to reduce the proportion of unsecured lending. While this means it is moving towards a lower ROA (return on assets business), it nevertheless augurs well for stability in long-term earnings.

The stock trades at 2.3X FY18 book. Any weakness could be a good starting point for accumulation.

Ujjivan Financial, on the other hand, has a much bigger micro finance book and took a bigger hit on earnings in recent times.

But secured lending is still a very small proportion of the loan book and hence the earnings volatility is likely to be higher in the medium term. Given the heightened provisioning requirement in the unsecured portfolio, Ujjivan is unlikely to turn meaningfully profitable in FY18. The stock currently trades at 2.3X FY18 book.

We do not rule out Ujjivan being acquired by a larger banking entity in the medium term. Hence, investors having patience to wait for such an event to play out could consider Ujjivan.

[“Source-moneycontrol”]